Risk Modeling Using ML

Machine Learning

5 MIN READ

January 31, 2023

![]()

What is Risk Modeling?

Risk Modeling is defined as a systematic approach used for the quantification of risk. It is associated with mathematical techniques and methods responsible for predicting the risk factors of business strategy. Risk modeling utilizes various techniques such as historical simulation, market risk, value at risk and extreme value theory for portfolio analysis and making forecasts to predict losses that can incur different risks in the future.

Key Problems With Risk Modeling

Sometimes, the risk model can be risky to use. When it comes to the qualitative phase, there are chances of causing programming or technical glitches. Also, qualitative data can be mismanaged because of human error.

Some Common Issues That Come With Risk Modeling:-

- Trusting the past data for future prediction- It is helpful to use historical data but we can’t assure that the same system will work for predicting future scenarios.

- Not providing accurate insight– Risk models need to combine with other benchmarks, market research and critical thinking which has no equation to manage.

- Can’t trust subjective topics Misalignment or bias can be one of the reasons for the risk model’s failure based on the company culture, including the people in charge, priorities, and people’s influence outside the organization.

- Insufficient or misinterpreted data– Risk models implementation needs expertise. Even if you have the right information, you need the skill and knowledge to use or interpret it.

Risk Modeling in the Financial/Banking Sector

In the financial industry, risk modeling is used for measuring, monitoring, and controlling credit risks, market risks, and operational risks. It has been used for different application areas including financial fraud-detection analysis, anti-money laundering, loans/lending approval algorithms, textual data analytics, a default prediction model, and many more.

How Machine Learning Surpasses the Risk Modeling Challenges?

Machine Learning applications have been used in various risk management processes.

In banking and financial institutions, Machine Learning techniques can help in reducing risk levels by analyzing huge amounts of data sources. Unlike traditional approaches where limited information like credit card scores is used, ML works well in analyzing the massive amount of personal information to reduce risk. Machine learning collects various insights and offers actionable intelligence to banking and financial organizations for making subsequent decisions. For example, Machine Learning taps into various data sources for customers who applied for loans and gives risk scores to them. With ML algorithms it could be easy to predict the customers which are likely to default on their loans and allow businesses to rethink or adjust their terms for every customer.

What Has Ksolves Covered So Far In Financial Risk Modelling Using ML?

This blog covers one of the many risk-modeling use cases that Ksolves has handled.

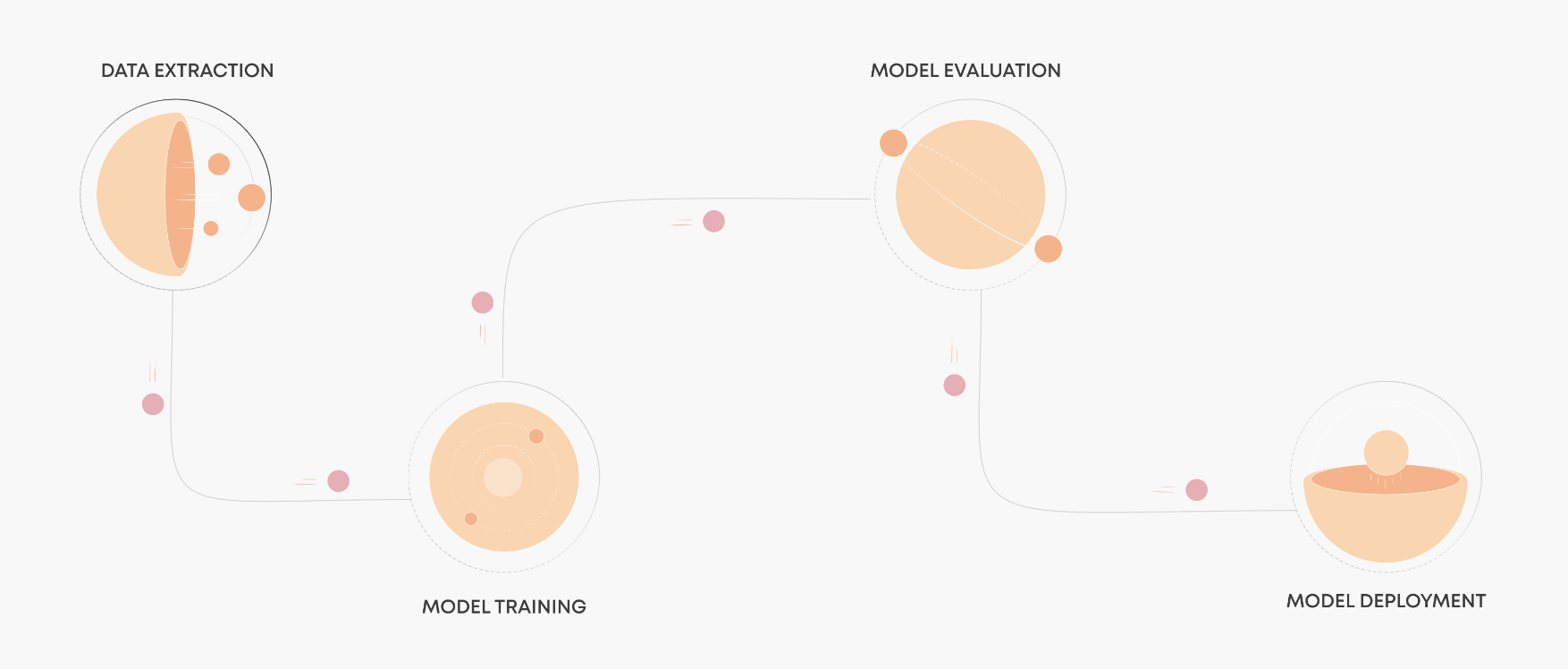

The lending company approves/declines the merchants’ applications who need a loan to expand their business on a daily basis. By implementing predictive modeling – our idea is to capture merchants who could default in the future when a deal is funded. Additionally, it is a renewal deal for the merchant, which basically means that the merchant has already taken the first loan and is now applying to take a second loan (renewal loan). This problem lies under the classification “supervised learning” category. We have built a classification model where a model outputs probability scores based on the predicted probabilities provided by the model output – one can tell if a merchant can default in the future or not. As a part of model building, we followed the state-of-the-art ML pipeline, depicted in the figure below.

Source: https://valohai.com/machine-learning-pipeline/

The dataset has merchant details with ~600 attributes for each merchant. These attributes contained all merchant historical information in the form of categorical and numerical values. In the next step, we prepared our data set for model building. This step involves data cleaning, imputing missing values using statistical approaches and attribute distribution, dropping down highly correlated features, and removing unwanted features. To train and evaluate models, data is divided into three sets: training, testing, and development. A state-of-the-art XGBoost classifier with extensive hyper-parameter tuning was built. Model performance was evaluated on validation data and checked for robustness on test data. Different business metrics were compared to get desirable probability ranges. In order to create a production-ready model for making further business decisions, statistical analyses were performed including decile and pentile analysis. As a result of this model, key decision makers of the management can create “Merchant Tiers” with different ROI.

Empower Your Business With Ksolves AI/ML Services

Artificial Intelligence and Machine Learning are having a significant impact across all industries, not just the financial/banking sector. Do you want to embrace the full potential of AI and ML for your business? If so, then Ksolves’ experts are here to help you.

Ksolves is a reputable AI and Machine Learning consulting firm that provides tailored services to meet the specific demands of clients’ businesses. We are backed by highly experienced and professional developers to provide the best AI/ML services that keep your business at the forefront of the market. If you want to know more about the kinds of use cases we have provided to our clients or need professional AI/ML expert services, contact our experts.

![]()

Frequently Asked Questions

Machine Learning is no longer a technology of the future. It is a core production capability powering fraud detection, demand […]

In recent years, machine learning (ML) has evolved from a niche technology into a vital tool across various industries. From […]

In today’s AI-powered world, data is not just fuel for machine learning, but it’s the foundation upon which intelligent systems […]

AUTHOR

Machine Learning

Mayank Shukla, a seasoned Technical Project Manager at Ksolves with 8+ years of experience, specializes in AI/ML and Generative AI technologies. With a robust foundation in software development, he leads innovative projects that redefine technology solutions, blending expertise in AI to create scalable, user-focused products.

Share with